Note: This article is being updated as and when deeper insights and feedback are received. Last updated on 19 March 2026.

Indian residential communities are generally managed as cooperative housing societies ( as largely seen in Maharashtra and Gujarat) or apartment owners associations or such similar arrangements. The broad concept is that home owners contribute to a common fund which is used for maintaining the common premises and for the provision of essential services such as water, electricity, security etc. These monthly maintenance contributions (MMC) vary with larger homes paying more as per their floor space. The management of these organisations are typically volunteers working pro-bono, while some of the larger and affluent ones employ facility managers or facility management companies to take on the day-to-day administration.

These managing organisations, generally referred to as Residents Welfare Associations (RWAs) or Apartment Owners Associations (AOAs) use the MMC collections for procuring goods such as power generator sets or hire services such as house-keeping for cleanliness. They are essentially non-profit organisations, though they may earn an income from investment of their collected funds or renting out a part of their premises. Such returns are ploughed back for the collective needs of the community and are not distributed as dividends to the members.

The question then is whether and how the Goods and Service Tax (GST) regulations are to be applied. It has been unequivocally accepted that the law of mutuality applies to RWAs. That is – the amount received from oneself cannot be considered income. This would imply that RWAs should not charge GST for services that have been purchased with their (home owners) own money since it would result effectively in double taxation. This is however countered by the ruling that RWAs are associations of persons which have a legal existence separate from its members, that they fall within the definition of “businesses” , and that they provide taxable services for a consideration. Hence, the current regulations require that GST needs to be charged to home owners, though in limited ways as we shall explain ahead.

What is Goods and Services Tax (GST) in the context of RWAs?

GST is the evolved form of Value Added Tax (VAT). In the VAT system, agencies in the supply chain pay their inward goods or service providers a tax component and pass this burden on to their customers along with an additional tax component in proportion to the value that they add. But this created a cascading effect with end-customers bearing a severe brunt. In the GST system, agencies in the supply chain can reduce some amount of their tax dues by deducting the inward goods tax (called Input Tax Credit or ITC) against the tax they apply on their outward supplies to the customer. This leads to lowered end prices and more equitable sharing of the tax burden.

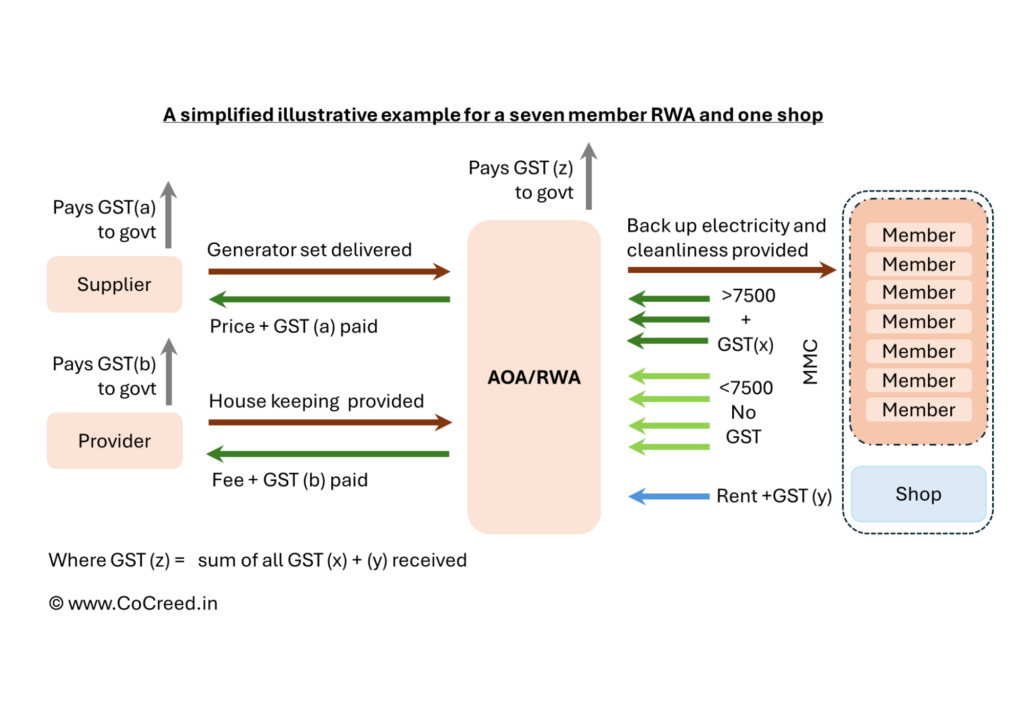

The current GST policy states RWAs which have an annual aggregate turnover of over Rs 20 lacs are required to register for GST. Turnover here means the value of services and charges, both taxable and exempt, charged to home owners. Registration is to be done under the Classification Group 99959 – Sub Group – 999598 – Home Owners Associations). These RWAs are then obligated to charge 18% GST to those member’s apartments which are charged more than Rs 7,500 as MMC. This GST is applicable on the complete MMC amount and not on just the amount which exceeds Rs 7,500. The policy also provides for a pro-rata discount of ITC to be deducted from the GST dues of the GST chargeable apartments. Shops which are run inside the apartment layout and pay GST on rent charged by the RWA also can be provided a pro-rata ITC if desired.

The diagram below provides a pictorial view of the GST process without the application of ITC:

We now take an example of how ITC can be applied and its benefit availed of ( vide Section 17(2) of the CGST Act read with Rule 42) for an AOA consisting of 100 apartments:

Category | Number of apartments | MMC (say) | Total turnover |

GST Non-liable apartments | 60 | ₹6,000 | ₹3,60,000 |

GST liable apartments | 40 | ₹8,000 | ₹3,20,000 |

| | | Total | ₹6,80,000 |

GST rules require that ITC can only be applied to GST liable (taxable) apartments and that too, based on the ratio of their turnover/charges to the total of 100 apartments.

In this case, the taxable turnover ratio = ₹3,20,000/ ₹6,80,000 = 47.06 %

Hence:

For input goods and services of value of = ₹ 1,00,000/-

GST @ 18% = ₹ 18,000/-

Total invoice = ₹ 1,18,000/-

Total ITC available = ₹ 18,000/-

ITC eligible = 47.6% x 18,000 = ₹ 8,740/-

Ineligible ITC ( to be reversed ) = ₹ 9,260/-

Now, GST law does not specify how the benefits of ITC are to be utilised by the AOA since it is a transaction tax, not a price-control mechanism. AOAs have the choice to pass the ITC benefits to GST-liable apartments or spread it across all ( simpler to administer) or retain the benefit in the corpus/sinking fund. The first option is the most defensible and transparent but requires additional accounting effort for recording and calculating ITC due to each of the eligible apartments. The calculation for each of the eligible apartments would be:

If MMC = ₹9,000

GST @18% = ₹1,620

Less ITC Benefit = (9,000/ 6,80,000) x 18,000 = ₹238

Net GST = ₹1,382

Total Payable = ₹10,382

It is generally noticed that rougly 50% of charged MMC is used for GST invoiced goods and services (water, electricity, property tax, direct staffing do not attract GST ). Hence in the above example, the ITC benefit could go upto even ₹800 or ₹900.

Shops which are charged rent by the RWA/AOA can also be accorded similar pro-rata ITC benefits by applying the ratio of the rent paid to the full turnover. However, this is not mandated and AOAs may choose not to.

How have apartment owners responded to this GST framework?

From the calculation in the example above and assuming ITC is not claimed, it is clear that apartments which are charged an MMC of ₹7,501 will need to pay a hefty 18% more than those charged ₹7,499. And this can appear unfair to many. It is hence likely that many RWAs try to ameliorate the situation by adjusting their expenditures among their apartments to keep them all below Rs 7,500. While this is indirectly unfair to the smaller apartments, the low levels of this shared burden (especially for large communities) and the sympathy factor may influence the RWA’s general bodies to accept this arrangement.

The question however, is whether such an adjustment is legitimate, even if it is accepted by a majority vote of its members?

Many RWAs may have also turned to reducing official amounts of MMC so as to protect their apartment owners. For example, some may bill water expenses separately. This is not entirely irregular, since water is typically not individually metered and supply of such basic necessities (electricity is another) has not been brought under the ambit of GST.

Another debatable area is the contribution towards the Corpus/Sinking fund, which forms a part of the MMC. Typically owners should pay GST on goods or services that they receive. But since the Corpus/Sinking fund is collected for a future need, owners may feel that they are being charged for something which they may never benefit from (especially if they intend to sell their apartments). Efforts to avoid GST may therefore lead to the ill-effect of RWAs reducing the contribution to Corpus/Sinking funds, thus opening the door to severe financial distress and disputes when large expenditures for major repairs arise in the future. Maharashtra, which has experienced hundreds of poorly maintained and unsafe residential societies, has mandated a minimum 0.25 % of construction cost per annum to be set aside in the Sinking fund solely with this aim.

Many cases have been filed in courts across different states of the country on these matters and many apartment federations have taken up these issues with governments. The outcomes of these may lead to changes in the policy. However, revenue departments are insistent on ensuring the current policy by charging stiff penalties for non-compliance, even in ambiguous situations which can lead to considerable discontent among RWAs. RWAs which are managed by members who are under-informed may also fall prey to the threat of heavy penalties, and pay amounts even when not fully justified.

What then should RWAs do?

The first step is obviously for members of the managing committees to make themselves aware of the nuances of the GST framework. The Indian Institute of Management, Bangalore and the Bangalore Apartment Federation have taken commendable steps to conduct a masterclasses for the treasurers of RWAs. Hopefully many more will be held, thus spreading the knowledge far and wide.

Secondly, a separate MMC head (and invoicing) could be created for collections for electricity, water bills and property taxes of individual apartments which are collected by and paid for by the RWA on behalf of members. These are exempt GST and are excluded from the aggregate turnover as well as the MMC amount which is subjected to the Rs 7,500 threshold. Electricity, water bills and property taxes of common areas area are also exempt GST but are to be included in the aggregate turnover and apply to the Rs 7,500 test. Hence these can be clubbed with other (non-exempt) charges in invoices to homeowners.

Thirdly, it is possible that many RWAs do not apply the ITC discounts to GST chargeable apartments, due to reasons such as a lack of GST invoices by suppliers or the non filing of GST returns (which credit the RWA with ITC), or a time delay between filing . If RWAs can overcome these barriers, the resultant discount from ITC can bring down the additional burden on GST chargeable members, to more reasonable levels. This will reduce the pressure by owners to avoid crossing the threshold. In this way, contributions to the Sinking fund can also be maintained at healthy levels and the future financial health of the RWA can be ensured.

Fourthly, if the Sinking fund is collected as a refundable deposit, it would be exempt from inclusion within the aggregate turnover as well as the MMC which is subject to the Rs 7,500 threshold. However, this will require separate invoicing, and its purpose and refundability needs to be declared in audit statements. If this refundable deposit is later used to pay for goods or services, then GST may apply at the time of expenditure, but not retroactively to the original collection. Hence, RWAs will need to tread carefully to maintain compliance and be willing to deal with the additional accounting burdeN.

Conclusion

RWAs are governed by councils of persons who are rotated and could have a temporary alliance. Hence extra caution needs to be taken to ensure decisions that are taken avoid negative effects at a later stage in the form of penalties. At the same time, there are genuine issues where clarity is lacking and which are being contested on fair grounds. RWAs must therefore attempt to assess the risks of entering litigative areas against full compliance and keep their members informed of them while taking decisions.

We hope you found this article helpful. Do you have any other angles to add or disagree with any aspect? We would love to receive your views and suggestions at Contact@CoCreed.in

Disclaimer: This article has been compiled and interpreted from information drawn from open sources and an AI platform and intends to provide clarity and a broad perspective. RWAs are advised to consult with professionals for detailed applicability as per regulations in their respective states. The views expressed are those of the author.